Hi there,

Welcome to the 107th edition of Heartcore Insights. Curated with 🖤 by the Heartcore Team.

If you missed the past newsletters, you can catch up here. Now, let’s dive in!

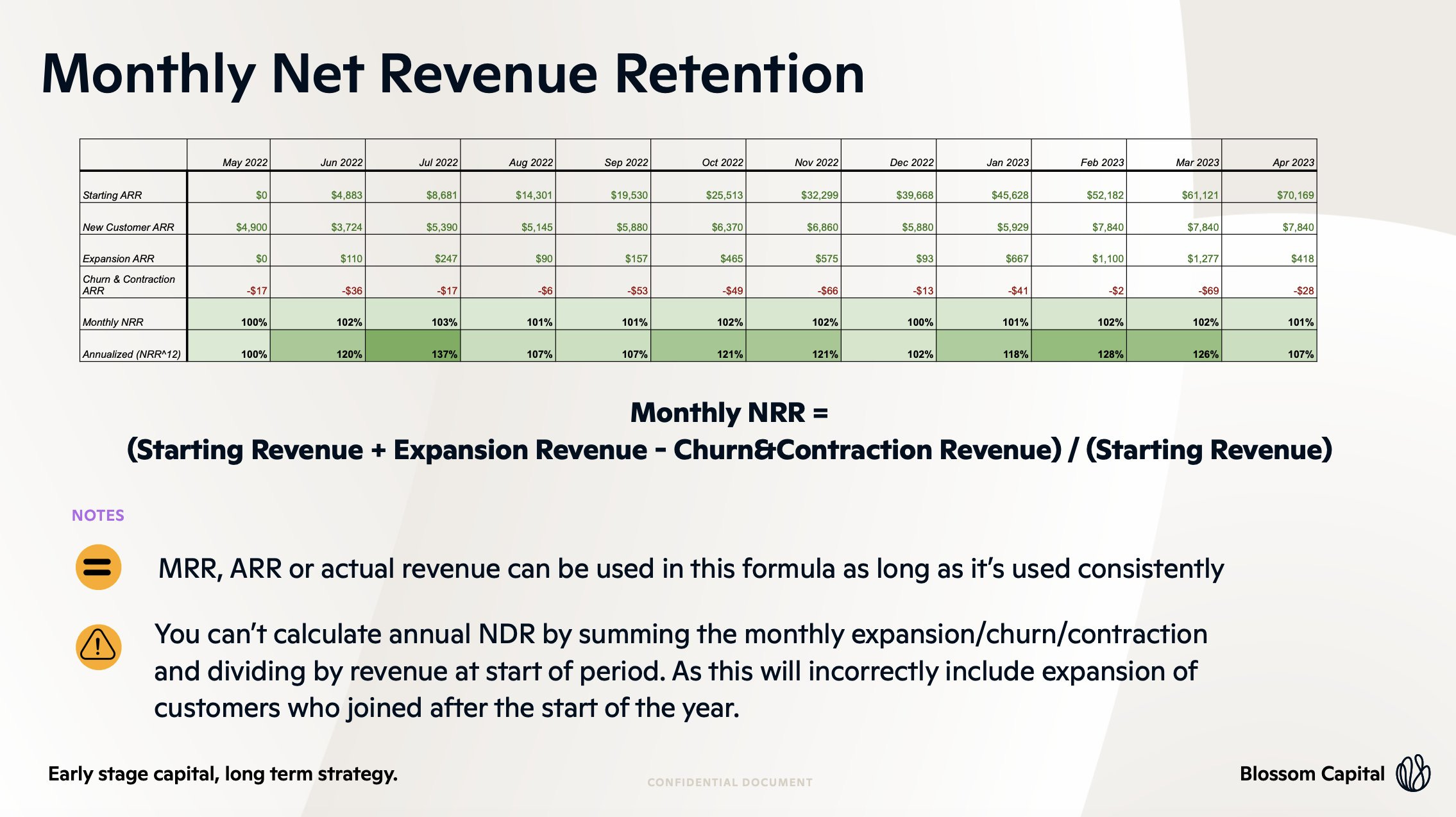

Field Guide to Net Revenue Retention - Blossom Capital

Net Revenue Retention is one of the most important metrics for tech companies, but it's also one that's often overlooked by early-stage founders.

NRR gives a measure of how much expansion revenue will be generated from existing customers. 120% NRR = on average a customer on €10k at the start of the year will end the year spending €12k.

The median public SaaS company generates 60% of its growth from NRR. While the impact of NRR seems small in the short term, it defines the trajectory in the longer term and can make a 2-3x difference in ARR by the time it comes to IPO:

These benchmarks are for typical early-stage (Seed-to-Series B) startups selling into mid to large-size enterprises. It's never too early to be thinking about NRR.

Even at Series A best-in-class startups have NRR of >140% It's also one of the key drivers of valuations at growth rounds (and increasingly early-stage rounds)

Public SaaS companies calculate NRR on an annual basis, but for an early-stage startup that's too long to wait to know whether it's working. Fortunately, there are a few ways to proxy the calculation on a quarterly and monthly basis so you have a much tighter feedback cycle.

Why Consumer Subscription Is So Hard, and What to Do About It

Why is consumer subscription hard?

Consumers are not rational, and it is thus very hard to predict who will churn vs. build habits around your product. Also, the amount made per customer tends to be a lot lower than B2B, and what makes this even worse is that even when you activate consumers into paying users who build habits, you do not increase the amount of money you make from them over time - net dollar retention, the best feature of a B2B subscription growth model, is not even present in a consumer subscription growth model.

The app stores take a significant percentage of subscriptions purchased through them and prevent alternate forms of payment to avoid that tax, so the margin structure of these consumer businesses are significantly hampered compared to their B2B counterparts.

Customer acquisition is much harder. Sales is out of the question. Secondly, every company uses paid acquisition to target its best potential customers first. And this usually works with healthy payback periods. But, to scale, the company needs to target more and more customers who look less like the core customer over time. They respond to the ads less, convert worse on the landing page into trials, convert from trials to subscriptions worse, and retain worse after subscribing.

How to solve the systemic challenges of Consumer Subscription?

The next generation of consumer subscription businesses tends to create product experiences that get better over time through either leveraging the data of their users or by offloading content creation costs to suppliers. Duolingo has done a masterful job of keeping retention high in a space with normally high churn because their lessons get better every day based on the feedback loop of their customer usage. We call that a data network effect. Spotify has exponentially more types of content (music, podcasts, video) and exponentially more artists than when it originally launched which attracts more listeners. That’s a cross-side network effect.

If network effects do not make sense for the type of product value you’re delivering, launching new products to monetize your existing customers better can ease the burden on customer acquisition. Calm was able to scale out its sleep stories product in a way that raised the retention rate of its meditation customer base as well as open up segments that were less interested in meditation. It turns out that selling a product solution for something people have to do everyday (sleep) has a much bigger market than a habit a small percent of the world does (meditation).

Most consumer subscription business treat their content as their proprietary secret sauce and keep it inside paid subscriptions. Much of the time, this means that content isn’t doing all it can to attract new customers. Masterclass is a great example of re-using a lot of the amazing content they sell in their courses and repackaging it for search engines as a taste of what the full courses offer. This has allowed a company that historically 100% grew via paid acquisition to diversify its acquisition sources, bring down payback periods, and find new audiences.

Creating a B2B offering allows you to target a new customer business with a new acquisition loop in sales that can acquire hundreds to thousands of people at the same time inside companies. Headspace and Calm have done a good job of expanding into this model as an expansion from their consumer roots.

The P9 Guide to Cohort Analysis in SaaS

DCTV Deep Tech Report

21 Ways To Shore Up Your Customer Success Org

Why startups do need strategy - despite what you've heard

AI & The Era of Ever-Evolving Employment

Engineering excellence

How to Do Great Work

Forecasting Lifetime Value - Challenges

🇪🇺 Notable European early-stage rounds

ScorePlay, a Portugal-based AI-powered content manager for professional sports, raises €4.5M with Seven Seven Six - link

Ivy, a German-based API for instant bank payments, raises €7M with Creandum - link

Rever, a Spain-based return management software for e-commerces, raises $7.5M with GFC - link

Supercritical, a UK-based company building a carbon removal market, raises $13M with Lightspeed/MMC/RTP - link

AutogenAI, a UK-based generative AI tool for writing bids and pitches, raises $22.3 million with Blossom - link

🇺🇸 Notable US early-stage rounds

Foraged, a US-based marketplace for wild and specialty foods, raises $2.7M with Bessemer - link

Cleanlab, a US-based startup developing automated data curation for boosting LLM performance and reliability, raises $5M with Bain - link

Maza, a US-based fintech providing immigrants with a tax identity to build financial history, raises $8M with a16z - link

Heard Technologies, a US-based financial back office for therapists, raises $15M with Headline/GGV - link

Apex Space, a US-based manufacturer of smallsat buses for commercial and government customers, raises $16M with a16z/Shield - link

Sound, a US-based music startup connecting artists and listeners, raises $20M with a16z - link

ElevenLabs, a US-based company developing AI voice synthesis software for creators and publishers, raises $21M with a16z/SVA - link

Bedrock, a US-based ocean mapping system, raises $25M with Northzone/Primary/Quiet - link

Captions, a US-based AI-powered video studio, raises $25M with Kleiner Perkins/a16z/SVA/Sequoia - link

Gardens, a US-based game studio growing the future of online social play, raises $31.3M with Lightspeed/Krafton - link

Preply, a US-based online tutoring platform, raises $42M with Horizon/Reach/Owl - link

🔭 Notable later stage rounds

Collective, a US-based fintech offering financial solutions designed for self-employed business owners, raises $50M with General Catalyst/QED/Gradiant - link

Render, a US-based cloud provider for apps and websites, raises $50M with Bessemer/General Catalyst - link

Volt, a UK-based open banking fintech, raises $60M with IVP/EQT/Fuel - link

Nothing, a UK-based consumer tech company developing digital technologies such as smartphones, raises $96M with Highland/EQT/GV - link

Redpanda, a US-based streaming data platform, raises $100M with Lightspeed/GV - link

Typeface, a US-based generative AI application to create personalized content creation for businesses, raises $100M with Salesforce/Lightspeed/GV/Menlo - link