✍️ WHAT CAUGHT OUR EYES

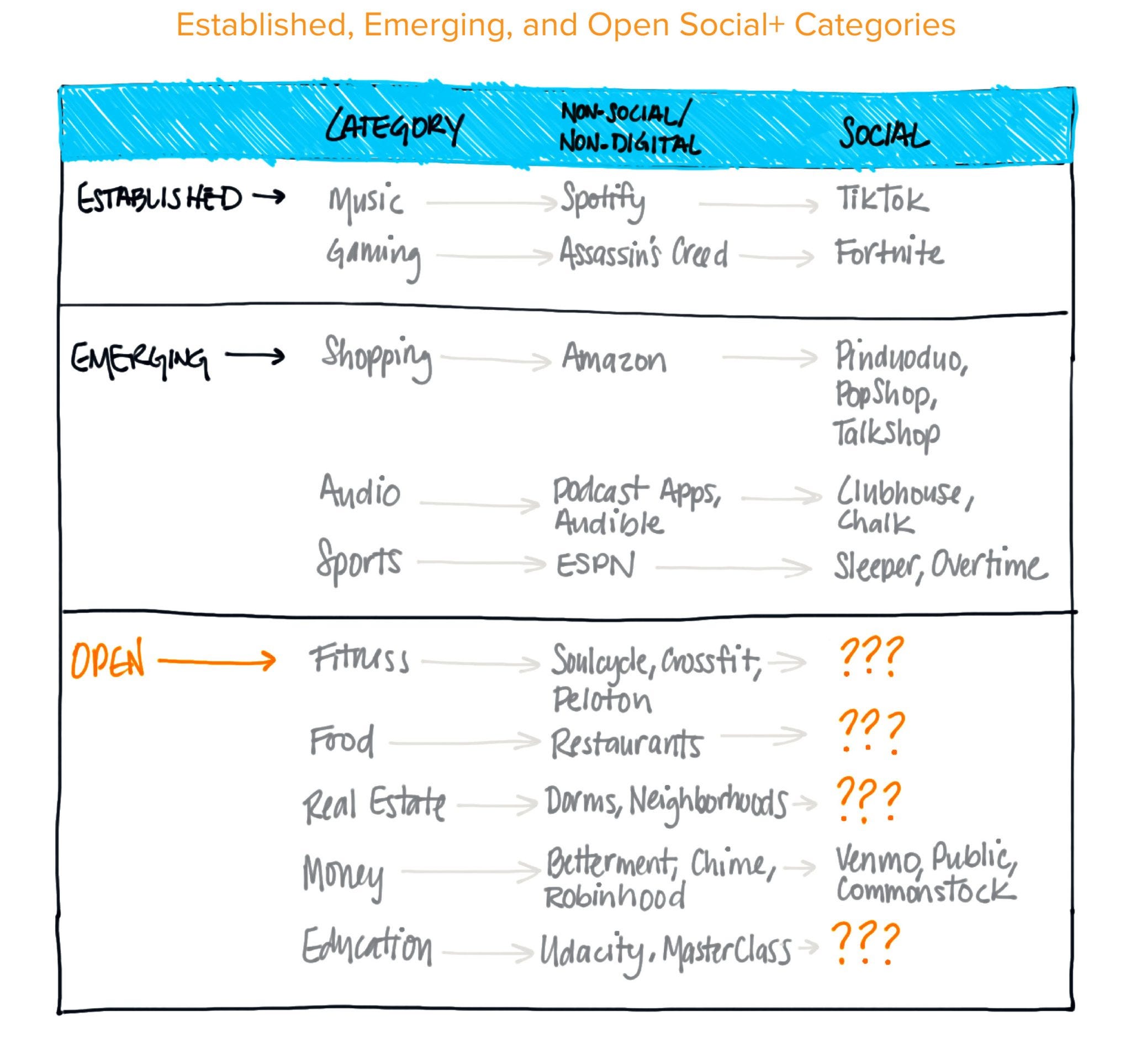

Community Takes All: The Power of Social+

Any product that has a social component baked in has asymmetric advantages over competing non-social products: better growth loops/engagement/retention/defensibility.

Just as every industry makes the crucial transition from analog to digital, nearly every category will eventually make the fateful transition from single-player to multiplayer.

Hallmarks of a Social+ company:

1. Unique/proprietary social graph that is purpose-built for that product: building a product on top of Facebook/Snap’s social graphs can be great, but the network belongs to them, not you. At the end of the day, those platforms can allow any other company to build the same product as yours (or, worse yet, auction off the right to access it).

2. The social graph is critical to the product: we’ve all used poorly designed products that take a fun single-player experience and thoughtlessly try to layer on a social dimension. Designing an annoying “invite a friend” pop-up, where it’s not wanted is not a Social+ product.

3. Peer-to-peer social engagement baked into the product itself: Social+ products feature authentic engagement between the users. In the fitness world, Strava creates true P2P engagement, while a company like Peloton is largely focused on engagement with instructors.

There are a lot of ways to go wrong building Social+ though: a Social+ product typically has both an interaction layer and a transaction layer.

From a product/marketing perspective, combining those two distinct tasks into a coherent experience can be a delicate balancing act.

But when the emotional layer and the transactional one are well-designed and mutually reinforcing, that’s when the magic happens.

Insider insights on how Doordash won in spite of being a late mover

Doordash initially tried to take over big cities.

Delivering in cities is hard: customers expect to pay less, drivers expect to be paid more, traffic is bad, parking is hard. Suburbs have better fundamentals and even more people.

Doordash shifted focus and launched in Long Island/New Jersey. They found instant PMF. Business skyrocketed and they were profitable in months. Over time, they reinvested those gains into the city to fight on their terms.

In food delivery, you can compete on: price, speed, selection, and quality.

Uber focused on speed. Doordash ran an analysis and found that as long as deliveries were <42mins, customers didn't really care how long they took. Uber focused on achieving sub 30min delivery times to their own detriment.

$DASH mostly focused on having the best selection (all the restaurants you want) and the best quality (make sure your food arrives on time, with everything in). That focus paid off.

Lastly, food delivery is a service business. It's run by and powered by people.

$DASH competitors focused on customers first; restaurants and drivers second.

$DASH decided to weigh all sides equally.

By treating merchants & dashers the right way, they became allies, not adversaries. Restaurants in particular felt they could trust DoorDash more vs. the competition. The rest is history!

TOP CONTENT:

Social strikes back

4 Signs You’re Building a World-Class Team

Wish S-1 analysis

How Neobanks Should Monetize Status Signaling

Headspace user onboarding analyzed

Mapping the Creator Economy

A new breed of founders using data to help the planet

Why Retention is the silent killer

How This 5X Founder Creates an Internal Culture With a “Crazy Focus” on Storytelling

👏 WHERE THE MONEY WENT

🇪🇺 Notable EU early stage Consumer rounds :

Quell, a UK-based at-home fitness gaming company raises $3M with Khosla/JamJar/YC/Social Impact Capital & Heartcore 🖤 - link

Simple, a Cyprus-based intermittent fasting app, raises €4.1M with Target Global/S16VC - link

Reface.ai, a Ukraine-based app for swapping faces in photos and videos, raises $5.5M with a16z - link

Finn.auto, a Germany based eco-conscious car subscription platform, raises €20M with White Star/HV/Picus/UVC & Heartcore 🖤 - link

🇺🇸 Notable US early-stage Consumer rounds :

Folx Health, a US-based digital health provider designed for the LGBTQIA+ community, raises $4.4M with Bessemer/Define/Polaris - link

MedArrive, a US-based startup that works with caregivers to provide in-home, non-emergency care, raises $4.5M with Kleiner/Define- link

Supergreat, a US-based social app for beauty enthusiasts, raises $6.5M with Benchmark/Thrive/TQ - link

🔭 Notable later stage Consumer rounds :

Getsafe, a Germany-based digital insurer, raises $30M with Swiss Re/EarlyBird/CommerzVentures- link

Sundae, a US-based real estate marketplace for distressed property, raises $36M with QED/Founders Fund/Susa/Prudence - link

GoHenry, a UK-based pre-paid debit card startup for kids and teens, raises $40M with Edison Partners/Gaia Capital - link

Luko, a France-based home insurance company, raises €50M with EQT/Accel/Founders Fund/Speedinvest - link

Step, a US-based mobile banking service providing educational resources for teens, raises $50M with Coatue/Stripe/Crosslink/Collaborative - link

Monzo, a UK-based fully-featured challenger bank, raises £60M with Novator/Kaiser/TED Global/Goodwater - link

Virta Health, a US/Finland-based developer of behavioral-focused diabetes treatment, raises $65M with Sequoia/Caffeinated - link

Calm, a US-based app for practicing deep meditations, raises $75M with Lightspeed/Insight/TPG - link

Catawiki, a Netherlands-based online marketplace for collectibles, raises €150M with Permira/Accel - link

Function of Beauty, a US-based maker of customizable hair and skincare products, raises $150M with L Catterton - link

🍭 Notable Consumer Exits

Metromile goes public via SPAC at a $1.3Bn valuation. Metromile is a US-based pay-per-mile auto insurance with backers including G Squared/Intact/Future Fund/Index/NEA - link

🖤 - HEARTCORE

Congrats to Finn.auto for raising €20M led by our friends at White Star Capital!

Congrats to Kaia Health for launching its unique solution to support pulmonary rehabilitation 🩺

Thrilled to have Quell join the Heartcore Family 🖤

Much 🖤 from Heartcore