Heartcore Consumer Insights 🚀

22/01/2021

✍️ WHAT CAUGHT OUR EYES

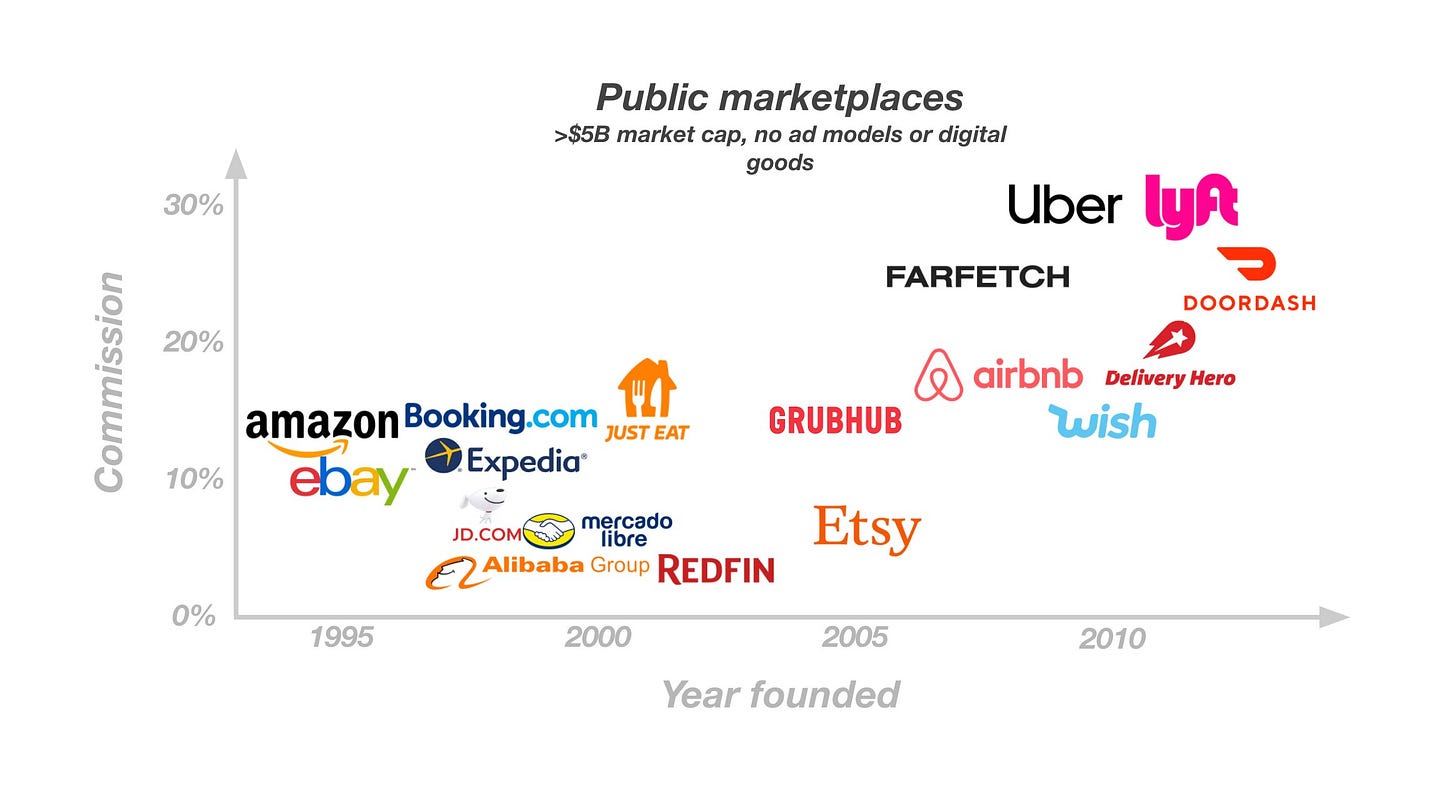

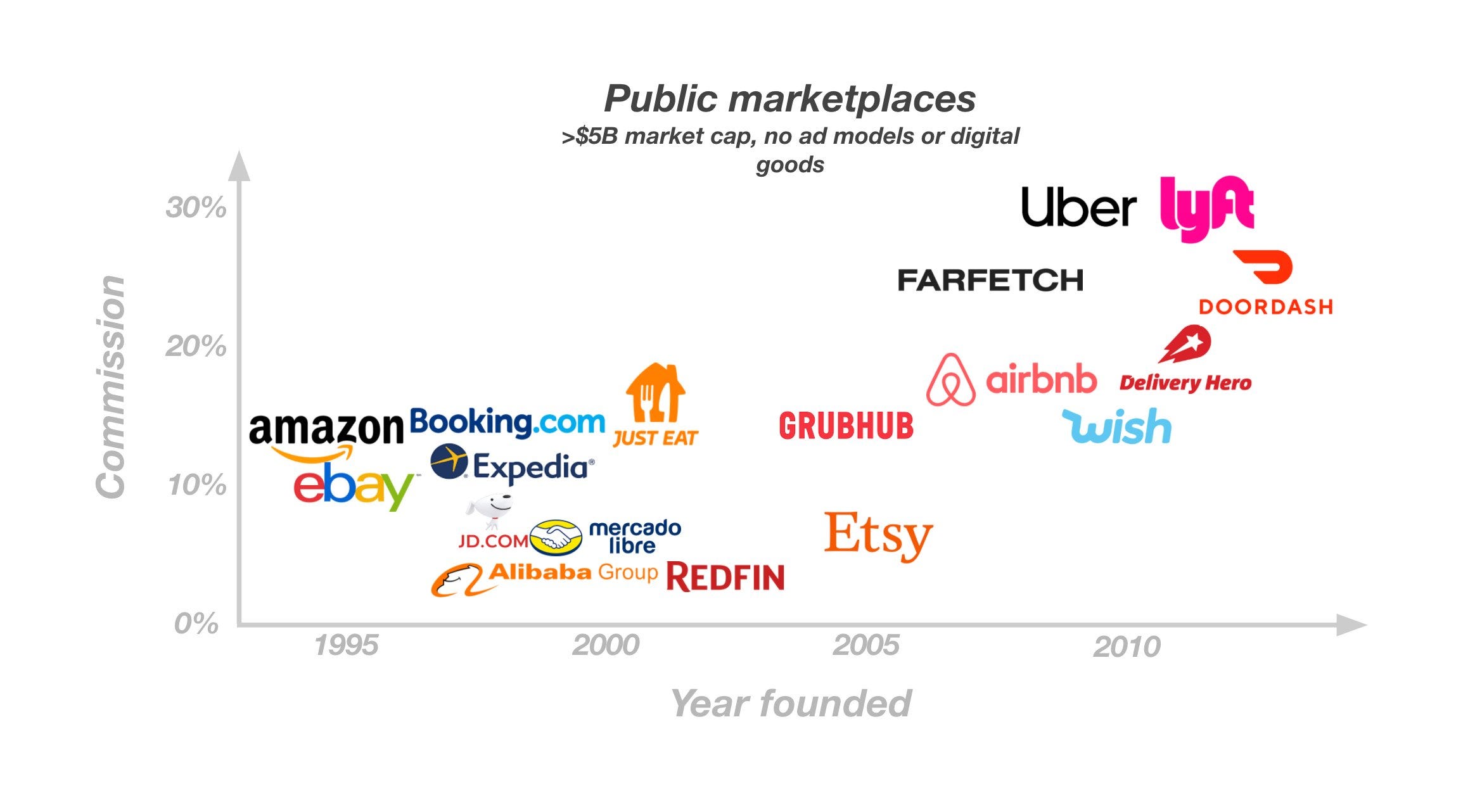

The future of marketplaces: coordination, capital, and creativity - Dan Hockenmaier from Reforge

When Airbnb and Doordash went public, they became two more data points in a long trend toward marketplaces with higher commissions doing more “work” to justify those commissions.

This “work” includes 3 things: (a) Coordination: making the product or service legible, matching buyers/sellers, establishing trust, (b) Capital: the full cost and risk of doing business, (c) Creativity: figuring out what to sell in the first place.

Light marketplaces are marketplace “1.0” like Zillow/HomeAdvisor that do just legibility/customer acquisition.

Vertically integrated "super suppliers" do everything. e.g. you can call Clutter a marketplace, but they're really a big, tech-enabled service provider.

In between these two, we have every type of marketplace under the sun. When a new marketplace model overtakes an old one, it is usually because they have taken on a new job that their suppliers used to do, and improved the customer experience. Let's look at a few examples:

Trust: eBay left a gap on trust that both GOAT and StockX exploited with their verification programs for collector sneakers.

Legibility: historically, local services marketplaces made intros and asked buyers/sellers to price the job. With their Instant Match product, Thumbtack is automating price discovery.

Risk: retailers previously relied on sales reps to help them understand what to buy wholesale. With access to more data, Faire is able to go a step farther and underwrite the transaction, offering net terms and free returns every time a retailer orders from a new brand.

Logistics: marketplaces are increasingly reaching farther into the supplier cost structure. By taking on responsibility for delivery, Doordash improved the customer exp. and expanded the restaurants they could bring onto the marketplace relative to Grubhub.

Creativity: In categories like transportation, personal services, & resale of existing goods, the thing being sold is a known quantity that rarely changes. Other industries have very high creative intensity (media, art, food, and much of consumer products and retail).

Marketplaces will ultimately figure out how to solve coordination problems like price discovery, matching, and supplier vetting and feedback.

Creativity yet is the only thing marketplaces won't entirely solve.

Here are a few implications for founders, operators, and investors:

If you’re building a marketplace model in an industry that doesn’t have one today, you must nail demand aggregation and legibility.

If you’re competing with an existing marketplace, look for an activity that your suppliers are currently doing today that you can do better to improve the customer experience.

Marketplaces in creatively intense categories will be more defensible. Categories where selection matters tend to have winner-take-all dynamics because the benefits of selection as you add supply take a long time asymptote, making it hard to catch up. On the other hand, those that compete mostly on speed/price/quality (Uber/Lyft) have network effects that asymptote quickly. This allows the market to support multiple competing marketplace models and destroys the profit pool.

The most important metrics to track when building a consumer subscription business - Lenny Rachitsky

B2C subscription businesses come in many shapes and sizes, but you can roughly break them down into three categories: Content, Software, and Physical Goods.

No matter the category, to succeed, a consumer subscription business needs to nail six things: (a) acquire new users sustainably, (b) get enough new users to quickly experience your value, (c) make sure enough users continue to find value, (d) make sure enough users decide to pay, (e) make sure enough users continue to pay, (f) be able to deliver the product/service profitably.

Important metrics to track for each type:

Software subscription businesses: (1). Activation rate: the percentage of free/trial users who hit a valuable milestone in the first X days after signing up (e.g. meditate, watch a show, listen to a song, find a match, sync a folder, etc.) (2). Intensity of engagement: L7/L30, (3). Conversion from free to paid: the percentage of free users who convert from free/trial to a paid subscription X weeks after signing up, (4). Cohort retention: the percentage of paid users who are still paying 1 month and 1 year later.

Content subscription businesses: (1). Cohort engagement: the percentage of users who are still doing something valuable (e.g. meditating, watching, listening etc.) X weeks after signing up. (2). Conversion from free/trial to paid: the percentage of free users who convert from free/trial to paid X weeks after signing up. (3). Cohort retention: the percentage of paid users who are still paying 1 month and 1 year later.

Physical goods subscription businesses: (1). Second-order retention: the percentage of users who don't cancel after their first order. (2). Contribution margin: incremental profit earned for each unit sold, subtracting all variable costs from a product’s price. (3). Cohort retention: the percentage of paid users who are still paying 1 month and 1 year later.

TOP CONTENT:

The future of physical retail

Global Consumer Spending in Mobile Apps in 2020

Deconstructing Among Us’ Twitter Strategy

The crazy year that was 2020 through the lens of the App Store charts

The Ultimate Guide to Unbundling Reddit

Internet 3.0 and the Beginning of (Tech) History

Flywheels And How To Create Content Communities

The Evolution of Social Media: Splitting Into Social and Media

👏 WHERE THE MONEY WENT

🇪🇺 Notable EU early stage Consumer rounds :

Bigger Games, a Turkey-based studio for casual puzzle games, raises $6M with Index/Play Ventures - link

Kenbi, a Germany-based modern nursing service for outpatient care, raises €7M with Redalpine/e.ventures/Partech & Heartcore 🖤- link

Weezy, a UK-based online supermarket that delivers in 15min, raises $20M with Left Lane/DN Capital & Heartcore 🖤 - link

🇺🇸 Notable US early-stage Consumer rounds :

Monument, a US-based digital treatment platform for alcoholism, raises $10.3M with VMG/Lerer Hippeau - link

Outer, a US-based outdoor furniture brand, raises $10.5M with Sequoia/Unlock - link

New Wave Foods, a US-based maker of a shrimp alternative, raises $18M with NEA - link

Landing, a US-based membership-based flexible living startup, raises $45M with Foundry Group/Greycroft/Maveron - link

🔭 Notable later stage Consumer rounds :

TaxBit, a US-based cryptocurrency tax automation software company, raises an undisclosed amount with PayPal/Coinbase -link

Too Good To Go, a Denmark-based startup that enables users to buy soon-to-be-wasted food from retailers, raises $31.1M with blisce - link

Cortilia, an Italy-based grocery delivery company, raises €34M with Red Circle/Five Seasons - link

Hipcamp, a US-based website for booking campsites, raises $57M with Index/Bond - link

CLARK, a Germany-based neo-insurance platform, raises €69M with Tencent/White Star - link

Curve, a UK-based banking platform that consolidates cards and accounts into one smart card and app, raises $95M with IDC/Fuel/Vulcan -link

Roblox, a US-based platform for creating and playing games, raises $520M with Altimeter/Dragoneer - link

🍭 Notable Consumer Exits

SoFi goes public via SPAC. SoFi is a US-based personal finance company, with backers including SoftBank/Silver Lake/IVP/DCM/Morgan Stanley - link

Twitter acquires Breaker for an undisclosed amount. Breaker is a US-based social broadcasting app, with backers including Arena/Zeno/Shrug - link

🖤 - HEARTCORE

Congrats to Kenbi for raising a €7M seed round.

Congrats to Weezy for raising a $20M round.

Travel is back. Congrats to TravelPerk for acquiring US-rival NexTravel.

GetYourGuide’s co-founder Tao Tao joins some of Germany’s tech leaders in founding 2hearts, a business community intended to support students and young entrepreneurs with immigrant backgrounds

Much 🖤 from Heartcore